Prediction Markets vs. States: The Fight Over the Meaning of 'Swap'

14 states, the CFTC, and billion dollar companies are in a knife fight over two phrases that define a 'swap'.

Prediction markets are built on binary yes-no questions. The fate of the industry rests on a binary question of its own: do sports event contracts like “who will win the Super Bowl” count as ‘swaps’?

If yes, then federal law preempts (i.e. overrides) state law and prediction markets can likely operate in all fifty states. If no, then sports event contracts are likely sports gambling, which is regulated by states, with all the licensing, taxes, and bans that come with that. Good luck building a venture-backed company if you need to get a gambling license in fifty states.

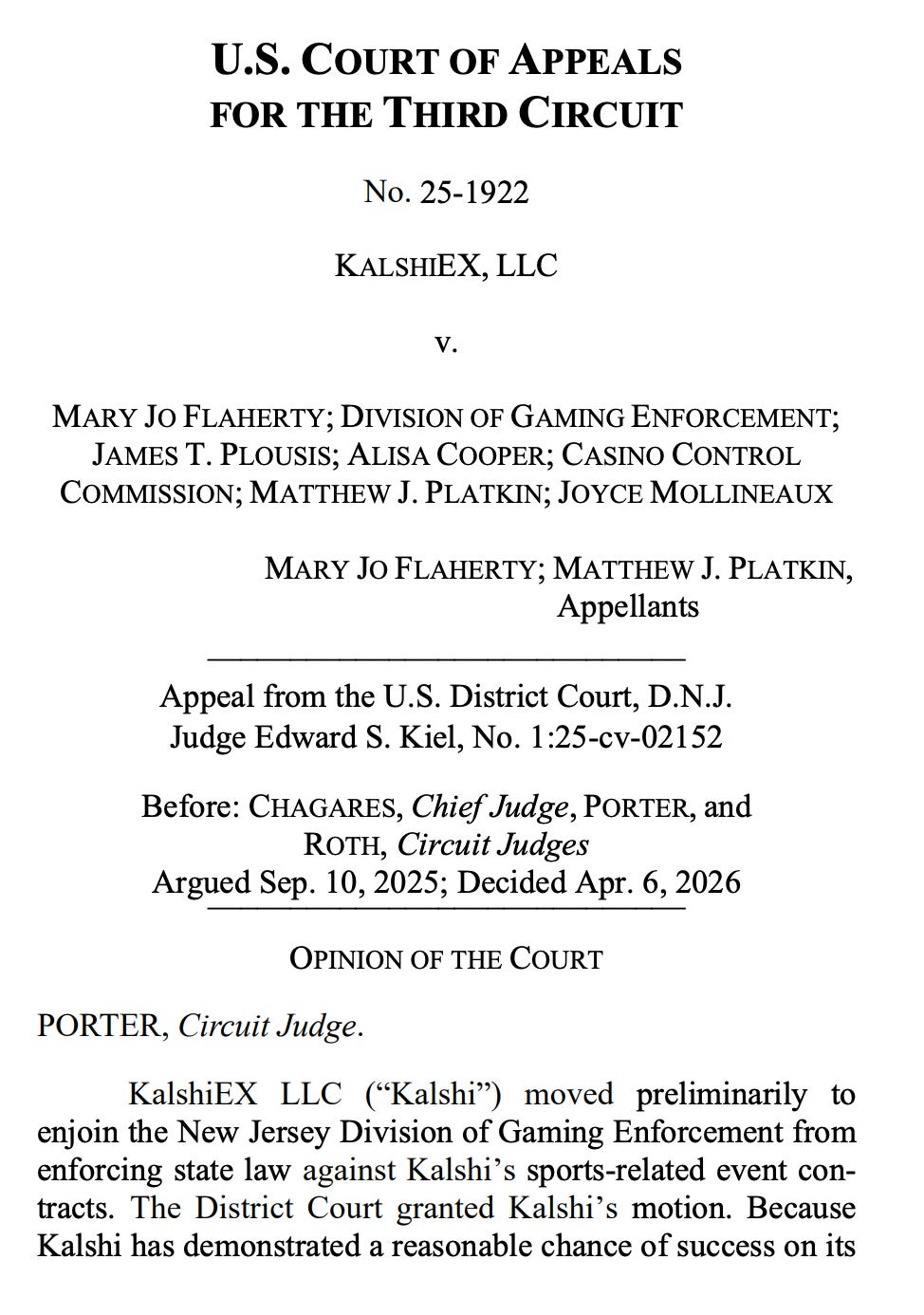

Today, in the highest-level ruling on this issue till date, the Third Circuit became the first appeals court to side with Kalshi. This is a big deal. Think of federal courts as a ladder: cases move through the district court, then appeals court, then the Supreme Court. Today’s ruling was at the second level. The Third Circuit stated that sports event contracts are swaps, so federal law under the Commodity Exchange Act preempts state law.

But the courts across the country are split.

Kalshi won in New Jersey (appeals court), Tennessee (district court), and Northern California (district court).

States won in Ohio (district court), Massachusetts (state court), and Nevada (state court).

The Commodity Futures Trading Commission is suing Arizona, Illinois, and Connecticut on Kalshi’s behalf. Washington state sued Kalshi last week, and Robinhood (which uses Kalshi to power its prediction markets) counter-sued Washington.

There are nineteen federal lawsuits pending.

After other appeals courts weigh in, this matter is likely headed to the Supreme Court in the next two years.

So What Exactly is a Swap?

Under section 1a of the Commodity Exchange Act, the term swap is:

“Any agreement, contract, or transaction ... that provides for any purchase, sale, payment, or delivery (other than a dividend on an equity security) that is dependent on the occurrence, nonoccurrence, or the extent of the occurrence of an event or contingency associated with a potential financial, economic, or commercial consequence”

In plain English, a swap is a deal where someone gets paid based on whether something happens or doesn’t happen, as long as that thing is connected with a potential economic consequence.

The term swap was added to the Commodity Exchange Act via the Dodd-Frank Act, which was written after the 2008 financial crisis to capture instruments like credit default swaps.

For example, Goldman Sachs owned mortgage-backed bonds but was worried that homeowners could default. Goldman paid AIG a regular premium; in exchange, if those mortgages defaulted, AIG would pay Goldman a large sum. The payment was triggered by an event (mortgage defaults) with an obvious financial consequence (Goldman losing money on bonds).

Even if an event contract qualifies as a swap for listing, the Commodity Exchange Act has a Special Rule that gives the CFTC the power to review and prohibit contracts that are “contrary to the public interest.” The Special Rule lists five categories of contracts that trigger heightened review: unlawful activity, terrorism, assassination, war, gaming, and a catch-all for “other similar activity” the CFTC deems is against public interest.

The threshold question is whether sports event contracts qualify as swaps. If they do, the CFTC has jurisdiction and the fight shifts to whether the Special Rule’s “gaming” prohibition applies. If they don’t, sport event contracts need to be regulated on a state-by-state basis.

It All Comes Down to Two Phrases

In the definition of ‘swap’, the bolded section below is what states, prediction markets, and the CFTC are fighting over the most:

“Any agreement, contract, or transaction ... that provides for any purchase, sale, payment, or delivery (other than a dividend on an equity security) that is dependent on the occurrence, nonoccurrence, or the extent of the occurrence of an event or contingency associated with a potential financial, economic, or commercial consequence”

There are two contentious phrases here:

“Associated with”

“Potential financial, economic, or commercial consequence”

“Associated with”

The CFTC and Kalshi state that “associated with” is a loose connective; it means “connected to” or “related to”, not “caused by” or “arising from”. The “association” to a potential financial consequence does not need to be strong, it just needs to exist. The Kalshi briefs cite examples of how sporting events are associated with economic consequences: Super Bowl host cities make billions in hospitality revenue, advertising markets shift based on which team is playing, and merchandise sales spike after team wins.

The states argue that “associated with” implies a meaningful, direct, or correlational relationship, one where two things rise and fall together. As New Jersey’s lawyer said, lung cancer is “associated with” smoking in this way. If any tangential economic effect is enough, then every event in the world is “associated with” some consequence, and every bet would be a swap. The funniest moment was when the New Jersey’s lawyer wrote that the CFTC was trying to regulate grandma’s bingo night:

“Either the CFTC did not exempt traditional gambling and sports betting because it does not think ‘swaps’ capture all gambling in the country, or the CFTC is funneling the bingo game at a rural senior-citizen home into its domain.”

However, most judges take the side of Kalshi and the CFTC on the meaning of “associated with”. They believe the word is broad enough. For example, in Tennessee, the judge ruled that “associated with” doesn’t require consequences to naturally follow or be “inherently connected” to the event.

“Potential financial, economic, or commercial consequence”

This phrase is driving the deepest split among the courts and is likely to determine the outcome of the case.

Kalshi and the CFTC argue that the word “potential” is intentionally broad. Congress could have used a stricter qualifier like “significant” or “material” but chose not to. It doesn’t suggest any minimum threshold for how large the financial consequence should be.

Kalshi argued that it screens and limits its contracts to those with “financially significant events”. It gave evidence of its partnership with Game Point Partners, an insurance company that helps sports teams and sponsors hedge performance bonuses.

The CFTC’s brief reiterated that sports events generate commercial activity such as hospitality revenue for surrounding businesses. Sportsbooks are also using Kalshi to hedge risk, suggesting the contracts have financial consequences.

The states argue that if “potential” means any theoretically possible economic effect, then the swap definition has no bounds: anything can be a swap. The Ohio court, which sided with the state, stated that if Kalshi’s account is true, then:

"all contracts for payment based on the outcome of a sporting event — all sports bets — would be forced onto DCMs like Kalshi and every sportsbook in the country would be put out of business."

States have highlighted inconsistencies Kalshi’s own previous arguments. In 2023, Kalshi sued the CFTC for prohibiting them from listing election contracts on the platform. The CFTC under the Biden administration argued that election contracts constituted “gaming” under the Special Rule of the Commodity Exchange Act, so they were against public interest and had to be prohibited. Kalshi argued that elections aren’t games and that the Special Rule prohibition applies to sports betting. “Congress did not want betting to be conducted on derivatives markets”, Kalshi argued. “A football game is a game”, they said, but an election isn’t. In September 2024, the DC district court ruled in Kalshi’s favor. But now, Kalshi is arguing the opposite: that sports event contracts are legitimate swaps with real economic consequences. Multiple states have highlighted the inconsistency in Kalshi’s position.

Kalshi’s response is that the Special Rule is discretionary, not mandatory. The Special Rule states that the CFTC may determine that contracts involving gaming are against the public interest, not that it must. Also, Kalshi makes a clever argument: the Special Rule proves that sports event contracts are swaps. Why would Congress write a special gaming review rule if sports contracts couldn’t be swaps? When asked what kinds of sports betting may not fall within the swap definition, Kalshi’s lawyer said that certain kinds of player props may not have sufficient economic consequence.

What Happens Next?

The whole case comes down to two phrases in how the Commodity Exchange Act defines a swap.

On “associated with”, Kalshi has the textual advantage: most judges think the word is broad enough. The connection between a sports event and its economic consequence need not be direct.

On “potential financial, economic, or commercial consequence,” the courts are split, and this is where the fight will be won or lost. The states believe the economic consequences need to be significant and Kalshi doesn’t meet the bar. Kalshi and the CFTC believe that any economic consequences would suffice, and that Kalshi meets that threshold.

The case will likely make it to Supreme Court in the next few years. It’s an unusual one that cuts across typical ideological viewpoints. The conservative justices are textual originalists, which favors Kalshi since the swap definition is broad. But they are also committed to federalism and states’ rights, which favors the states.

The last time the Supreme Court weighed in on sports betting, it sided with states’ rights and struck down PASPA, the federal ban on sports betting. That ruling led to distinct state-by-state gambling regulations, the same ones that the states are now fighting to protect.

The liberal justices are typically pro-federal regulatory authority but skeptical of financial industry arguments and sympathetic to consumer protection.

There isn’t a clean 6-3 split here.

But my assessment is the Supreme Court will side with Kalshi and the CFTC because the definition of ‘swap’ in the Dodd Frank Act was intentionally broad. In the PASPA case, there was no federal regulatory body to oversee the sports betting ban, so states’ rights won over federal preemption. But in this case, there is a federal body (CFTC) that has a clear mandate to regulate swaps, which under the broad definition by Congress, includes sports event contracts.

14 states and the CFTC fighting over two words in a definition is honestly fascinating. thank you for the update!

!!!